Construction costs across the Gulf Cooperation Council (GCC) rose sharply during the first half of 2026, as geopolitical tensions, shifting trade policies and supply chain disruptions pushed up prices for key building materials, according to new market intelligence from engineering consultancy AESG.

The firm’s Q2 2026 Middle East Market Intelligence Report, based on tender return data from Q4 2025 to Q2 2026, shows that while the region’s construction sector remains highly active – with an estimated $951 billion worth of projects under execution according to MEED – developers and contractors are increasingly having to navigate a more volatile cost environment.

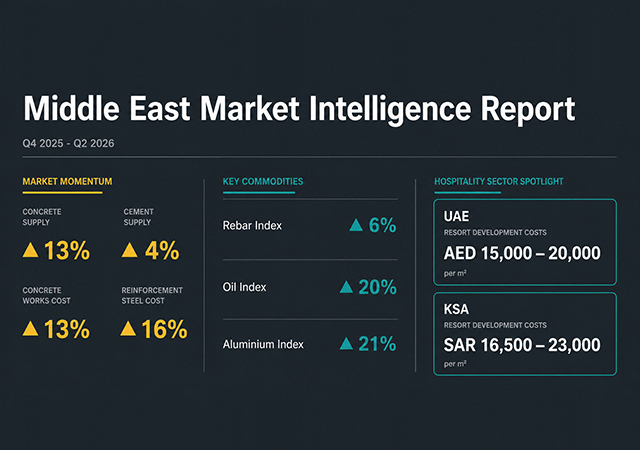

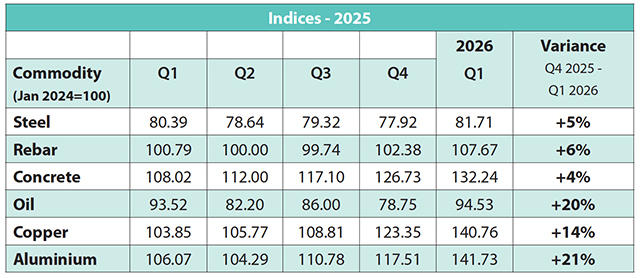

Commodity markets have been a major source of pressure. Aluminium prices climbed 21 per cent since late 2025, while copper surged 14 per cent to approximately AED46,000 ($12,526) per tonne, supported by rising demand from artificial intelligence infrastructure and data centre developments. Rebar prices increased six per cent to AED2,520 per tonne between Q4 2025 and Q1 2026, while concrete supply rates rose 13 per cent and cement prices increased four per cent over the same period.

Oil markets added further uncertainty. Brent crude fluctuated from around $70 per barrel in early March to above $110 during periods of heightened regional tension, feeding directly into transportation, logistics and energy-intensive construction activities. Stainless steel was one of the few materials to buck the trend, declining from AED9,500 per tonne to AED7,500 per tonne as increased nickel supply and weaker Chinese industrial demand weighed on prices.

Concrete works have increased by around 10 to 15 per cent since Q4 2025, while reinforcement steel costs have risen by 16 per cent, reflecting the broader shift in global commodity and logistics markets.

Despite these headwinds, AESG says the underlying fundamentals of the GCC construction market remain robust.

“The data we are seeing reflects a market absorbing real and sustained cost pressure, but one that retains the capacity and ambition to deliver,” says Saeed Al Abbar, Chief Executive Officer of AESG. “These findings are a prompt for rigour, not retreat. Developers who engage now with accurate, up-to-date benchmarks will be far better placed to make confident investment decisions and protect project viability as conditions evolve.”

AESG forecasts overall tender price inflation of between five to eight per cent in the UAE and four to seven per cent in Saudi Arabia during 2026, although pricing volatility remains “notably elevated” across façades, MEP systems, structural steel and specialist imported packages.

The report also highlights a weakening macroeconomic backdrop. The World Bank has revised its GCC economic growth forecast from 4.4 per cent in 2025 to 1.3 per cent in 2026, reflecting what AESG describes as a broader recalibration of global energy routes, trade flows and financial markets.

Data centres emerged as the region’s most pressured construction segment, with demand for power-intensive facilities creating acute constraints across MEP trades, cooling systems and specialist technical labour. AESG rates both market activity and pricing pressure in the sector as exceptionally strong. Infrastructure and logistics and industrial developments were also identified as high-activity sectors facing significant cost escalation.

Meanwhile, residential and commercial office projects continue to experience more moderate pricing movement.

AESG estimates construction costs for mid-rise residential apartments in the UAE at AED6,000-10,000 per sq m, rising to AED7,500-12,000 per sq m for high-rise developments and AED12,000-16,500 per sq m for upscale hospitality assets and AED15,000 to 20,000 per sq m for resorts.

The report points to a notable shift in contractor behaviour as firms become increasingly selective about the projects they pursue. Contractors are showing greater reluctance to accept fixed-price risk, resulting in fewer tender submissions, shorter bid validity periods and higher allowances for uncertainty. The frequency of force majeure notices, extensions of time and prolongation claims has also increased, driven by material price escalation, shipping delays and energy-related cost pressures.

As a result, many developers are moving away from traditional lump-sum procurement models in favour of phased awards, framework agreements and provisional sum arrangements. AESG notes that several major developers have already established preferred supplier and contractor frameworks to secure more favourable pricing for high-volume materials such as concrete and reinforcement.

UAE/Saudi cost comparison

Hospitality projects remain among the most expensive asset classes in the region. Resort developments in the UAE are currently benchmarked at AED15,000-20,000 per sq m, while comparable projects in Saudi Arabia range from SAR16,500-23,000 per sq m. AESG says feasibility studies completed as recently as late 2025 may need to be revisited to account for the recent uplift in construction costs.

The report also highlights the growing divergence between UAE and Saudi construction cost profiles. Saudi Arabia’s benchmarks remain notably higher across residential villa and hospitality developments, reflecting greater dependence on imported materials, longer supply chains and the demands created by the kingdom’s unprecedented giga-project programme.

According to AESG’s cost management team, led by Regional Director Daniel King, Senior Associate Director Jarryd Terblanche and Principal Cost Manager Harry Ross-Dreher, access to resilient supply chains, specialist subcontractors and established procurement networks is becoming an increasingly important differentiator between successful and delayed projects. The report notes that the Saudi Construction Price Index rose two per cent year-on-year.

The broader macroeconomic context reinforces the importance of robust project planning. Third-party forecasters have adjusted GCC growth projections for 2026 in line with shifting global market conditions. For Saudi Arabia, in particular, AESG’s data supports the ongoing approach of pressure-testing assumptions against current benchmarks, an approach that positions developers to move decisively as market conditions continue to evolve.

Underpinning this activity, AESG’s data shows supply keeping pace with demand. Cement supply increased by four per cent and average concrete supply by 13 per cent between Q4 2025 and Q2 2026, a sign of a market that is active, competitive, and well-resourced.

“The region’s infrastructure ambitions, population growth dynamics, and long-term tourism and economic diversification goals have not changed. What has evolved is the cost environment in which those ambitions are currently being executed. Against a backdrop of nearly $1 trillion in active GCC construction, the fundamentals of this market are not in question. What this data tells us is that the developers who move with the right benchmarks today will be the ones best positioned to deliver on those commitments tomorrow,” concluded Al Abbar.