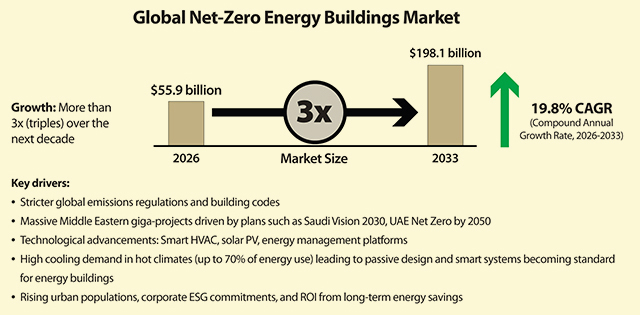

The global market for net-zero energy buildings is expected to more than triple in value over the next decade, reaching $198.1 billion by 2033 as Middle Eastern giga-projects and stricter global emissions regulations accelerate the shift toward sustainable construction.

According to a report on the Net-Zero Energy Buildings (NZEB) market by Persistence Market Research, the sector – valued at roughly $55.9 billion in 2026 – is expanding at a compound annual growth rate (CAGR) of 19.8 per cent. The growth is underpinned by a surge in demand for structures that generate as much energy as they consume through integrated solar power and high-efficiency cooling systems.

While Europe currently holds a leading 31.4 per cent market share, analysts point to the Middle East as a critical growth frontier. In a region where cooling can account for up to 70 per cent of a building’s energy use, the adoption of “passive design” and smart HVAC technology is moving from a niche luxury to a regulatory requirement.

While Europe and East Asia currently hold significant market shares, the Middle East and North Africa (MENA) region is emerging as a high-growth corridor driven by ambitious giga-projects and national visions such as Saudi Vision 2030 and the UAE’s Net Zero by 2050.

Net-zero energy buildings are designed to generate as much energy as they consume annually through energy-efficient design and on-site renewable energy systems, helping reduce carbon emissions and operating costs. These buildings integrate technologies such as solar photovoltaics, advanced insulation, smart HVAC systems, and energy management platforms to balance energy consumption and generation.

As urban populations grow and climate commitments intensify, construction firms and property developers increasingly adopt net-zero concepts to reduce long-term operational costs and meet regulatory requirements.

Growth is fuelled by stricter energy-efficiency regulations, increasing renewable energy adoption, and rising demand for sustainable construction practices worldwide.

According to the study:

• Europe leads the global market with around 31.4 per cent share, supported by strict building decarbonisation regulations and large-scale renovation programmes across the European Union.

• East Asia accounts for nearly 23 per cent of the market, due to rapid urbanisation and strong renewable energy manufacturing capabilities.

• Government initiatives promoting Zero-Emission Building standards and green construction incentives are accelerating adoption of net-zero building technologies worldwide.

• Increasing integration of solar photovoltaic systems, smart HVAC technologies, and building automation platforms is improving energy efficiency in residential and commercial structures.

• Large construction projects, smart city programmes, and corporate sustainability commitments are driving investment in net-zero commercial and residential buildings globally.

The global transition toward carbon-neutral infrastructure is a major driver of the net-zero energy buildings market. Governments worldwide are implementing stricter building energy codes and decarbonisation policies to reduce emissions from the built environment. Buildings account for a significant share of global energy consumption and carbon emissions, making energy-efficient construction a priority for climate action strategies.

Construction firms increasingly integrate energy modelling software during the design phase to ensure buildings meet net-zero standards before construction begins.

Many countries have introduced regulations requiring new buildings to meet near-zero or zero-energy performance standards. For instance, European policies under the Energy Performance of Buildings Directive encourage high-efficiency structures with renewable energy integration. Similar initiatives are emerging across North America and Asia as governments aim to meet long-term climate targets.

Developers increasingly incorporate energy-efficient materials, passive design techniques, and renewable power generation systems into building projects. Solar photovoltaic panels, geothermal heating systems, and energy-efficient insulation technologies are commonly integrated into new residential and commercial structures.

The economic benefits of net-zero buildings further support adoption. Although initial construction costs can be higher, long-term energy savings and government incentives improve return on investment (ROI) for property owners and developers. As sustainability becomes central to urban planning, net-zero buildings are emerging as a standard rather than a niche solution.

Rooftop photovoltaic panels generate electricity directly at the building site, reducing dependence on grid power.

Rapid adoption of technologies

Technological advancements in renewable energy systems and smart building management solutions are accelerating the adoption of net-zero energy buildings worldwide. Solar photovoltaics, energy storage systems, and intelligent building automation platforms enable structures to generate, store, and optimise energy consumption more effectively.

Solar energy plays a particularly important role in net-zero buildings. Rooftop photovoltaic panels generate electricity directly at the building site, reducing dependence on grid power. Combined with battery storage systems, these technologies allow buildings to balance energy production and consumption over time.

Advanced building management systems further enhance efficiency by monitoring energy usage in real time. Sensors and IoT-enabled devices track temperature, lighting, and occupancy patterns, automatically adjusting systems to minimise energy waste. Smart HVAC systems and automated lighting controls significantly reduce energy consumption in commercial and residential buildings.

Construction firms increasingly integrate energy modelling software during the design phase to ensure buildings meet net-zero standards before construction begins. Corporations are also adopting net-zero buildings to meet sustainability commitments and ESG reporting requirements. Large companies are investing in energy-efficient office spaces and industrial facilities that minimise environmental impact while reducing long-term operational costs. As renewable energy technology becomes more affordable and building automation systems improve, net-zero construction is becoming more accessible for developers worldwide.

Segmentation Insights

Equipment represents the leading component segment, accounting for approximately 74 per cent share, reflecting the capital-intensive infrastructure required to achieve net-zero building performance. This includes HVAC systems, renewable energy systems, energy storage, lighting solutions, and high-performance building envelope technologies. Deployment of advanced heat pump–based HVAC solutions and integrated solar systems continues to strengthen this segment’s dominance.

Meanwhile, solutions and services represent the fastest-growing component segment, driven by the increasing need for system integration, building energy management platforms, and performance monitoring services. The expansion of digital building management ecosystems and energy-as-a-service models is accelerating demand for these software- and service-based solutions.